The Hidden Cost of Upgrading: Why Your “Cute” House Might Be the Smarter Play

Let’s talk about houses. More specifically, the quiet, unspoken pressure to constantly upgrade them.

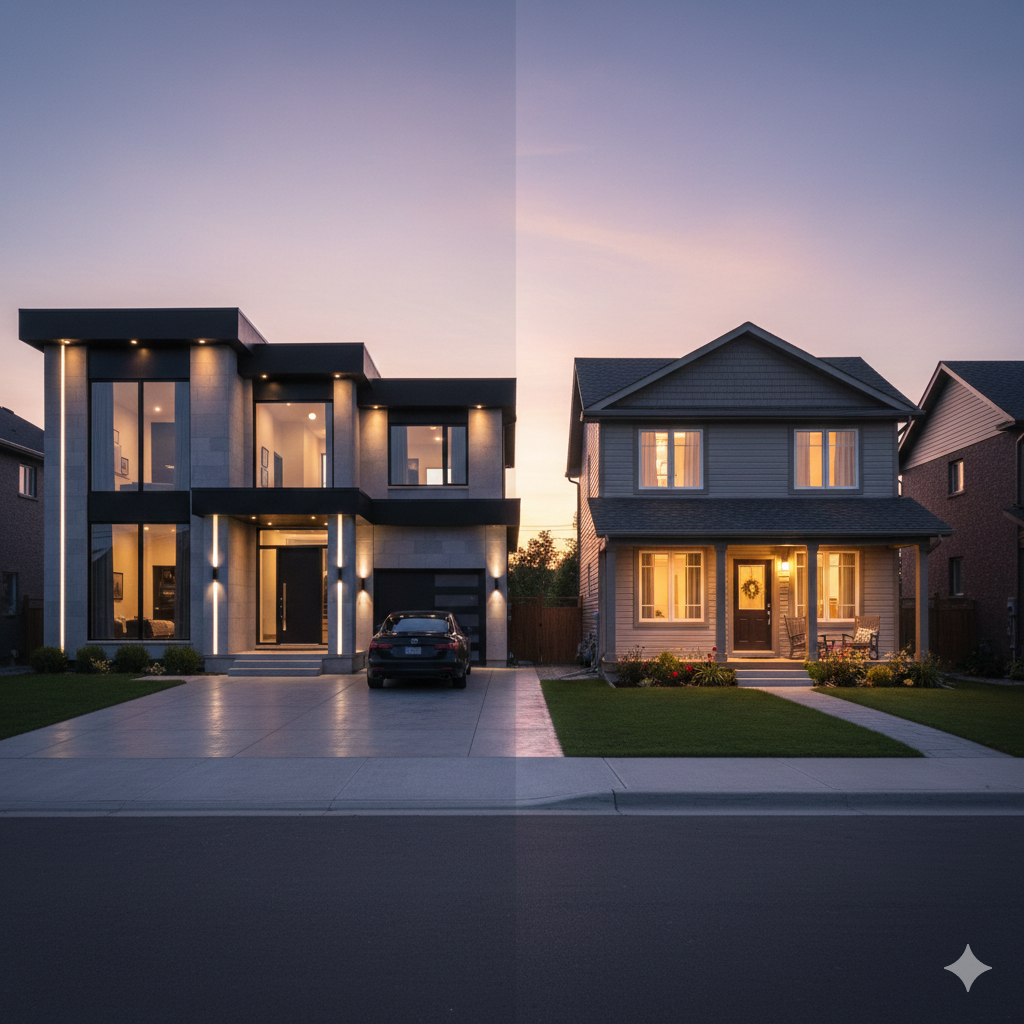

You’ve seen it play out. Your friend bought a $300,000 starter home in their late 20s. Two years later, they “moved up” to a $600,000 place in a better school district. Five years after that, they landed in a $950,000 house with a big kitchen island, a three-car garage, and a mortgage to match.

It all looks like progress. Like success. Like doing everything right. But under the surface, there’s a different story.

The Upgrade Cycle No One Talks About

Here’s what happened behind the scenes:

- They rolled over their equity each time, so they always had a mortgage.

- They reset their 30-year amortization, not once, but three times.

- They paid realtor commissions and legal fees every time they moved.

- They tripled their property taxes, utilities, and insurance costs.

And now, a decade later, they have:

- $650,000 in mortgage debt

- $300,000 in paper equity

- And jokes about your “cute little house”

When Bigger Means Slower

What your friend doesn’t realize is that while they were chasing square footage, you were quietly building something else.

You stayed in the starter home. You resisted the pressure to “move up.” You took the difference in cost, the lower bills, the lack of moving fees, the absence of renovation projects, and used it to build a cushion. Maybe you invested more. Maybe you paid down debt. Maybe you simply bought yourself peace of mind.

And now, instead of staring down 25 more years of mortgage payments, you’re on track for financial freedom in your late 30s or early 40s.

That’s 20 years earlier than most. No upgrades required.

The Social Pressure to “Move Up”

There’s an unspoken rule in modern life: as your income goes up, so should your lifestyle. A bigger house. A nicer car. More expensive vacations.

It’s a game of appearances, and many people play it without realizing the long-term cost. In the case of homeownership, those costs are magnified. A bigger home doesn’t just mean a bigger mortgage, it means bigger bills, more upkeep, more furniture, more stress.

Worse, it resets your timeline. Every time you refinance into a new 30-year mortgage, you push the finish line further away. It’s a form of lifestyle debt disguised as progress.

Why “Settling” Might Be the Smartest Move You Make

Here’s the thing: nobody’s saying you shouldn’t enjoy your home. Comfort, pride of ownership, and happiness matter. But there’s a difference between upgrading intentionally and upgrading out of habit, pressure, or comparison.

That “cute” house your friend teases you about? It’s the reason you sleep better at night. It’s the reason your stress is lower, your freedom is higher, and your future is closer.

You didn’t “settle.” You strategized.

And that choice, quiet, unflashy, and often invisible to others, is what might set you up for the kind of freedom that most people never reach.

A Final Thought

Upgrading isn’t bad. But defaulting to upgrade mode without considering the long-term implications can quietly drain your wealth, your options, and your time.

The best financial decisions often don’t come with applause. They come with simplicity. With control. And with the slow, steady realization that you don’t need more house to build a better life, just a better plan.

Want to run the numbers on how your housing decisions affect your future? Optiml can help you build a plan that prioritizes freedom, not just square footage.