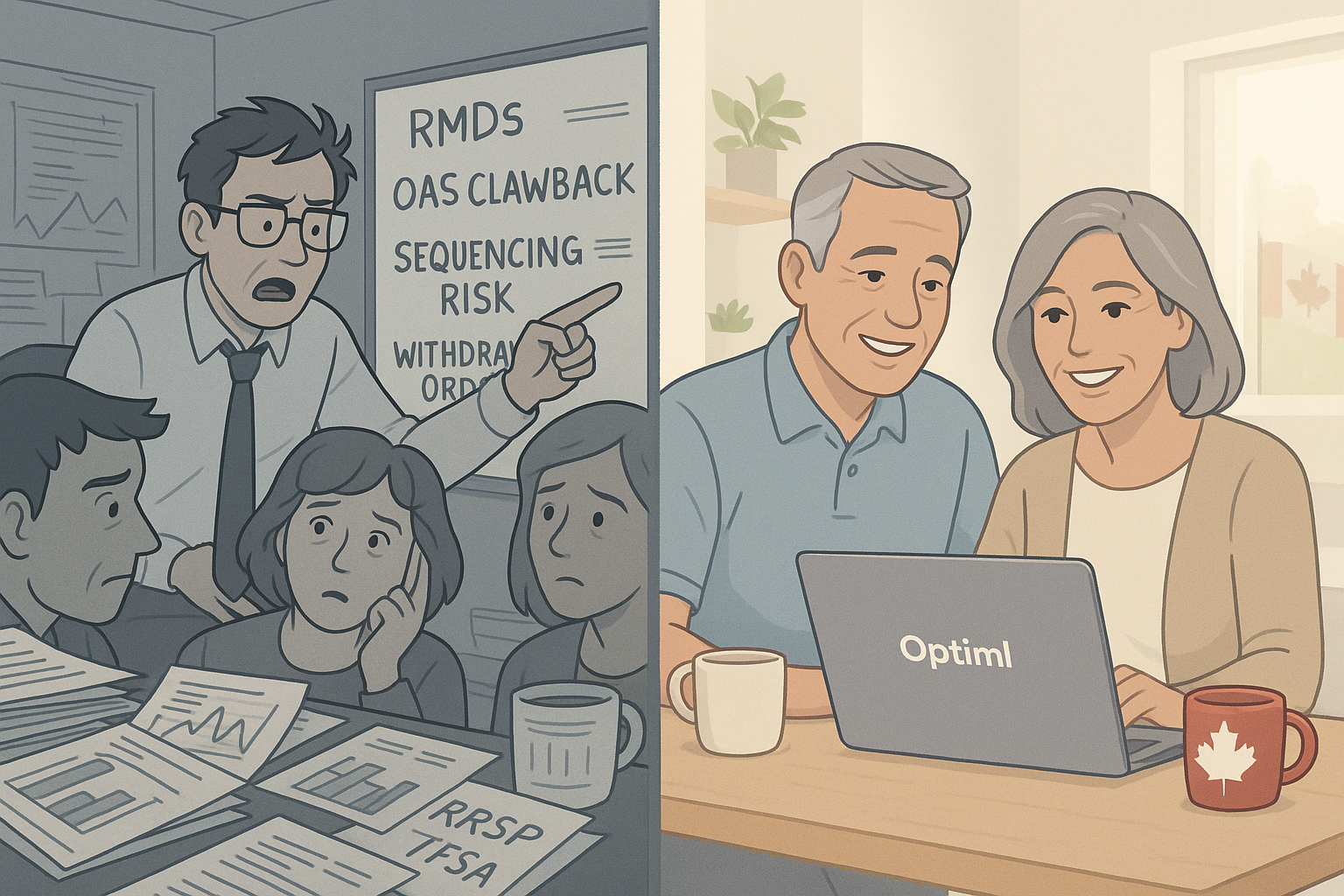

The financial industry loves making retirement sound harder than it is. Ever heard of “sequencing risk,” “stochastic modelling,” or “liability-matching”? These buzzwords aren’t there to help you understand, they’re often used to make you feel like you can’t (or shouldn’t) plan your retirement without handing over total control.

Here’s the truth: the decisions around retirement are simple. The math behind them isn’t. And that’s exactly what Optiml is built to solve.

What Retirement Planning Really Comes Down To

You only need to answer five questions to build a solid retirement plan:

- When should I start CPP and OAS?

- How much can I safely spend each year?

- What’s the most tax-efficient way to withdraw from my accounts?

- How can I avoid big tax surprises or OAS clawbacks?

- How do my real estate, business, inheritance, or life insurance fit in?

Simple to ask but complicated to calculate. These choices interact like a Rubik’s Cube. Twist one, the others shift. That’s why doing this in your head or in a spreadsheet often leads to costly mistakes.

The Real Challenge: Complex Interactions

Here’s what you’re really trying to juggle:

- Income sources are taxed differently (RRSP, TFSA, non-registered)

- OAS and GIS have clawback thresholds

- Markets don’t return 6% every year in a straight line

- Inflation erodes your spending power over decades

- RRSPs become RRIFs with minimum withdrawal rules

Add in a spouse, provincial tax rates, CPP start dates, and a possible inheritance, now you’re tracking thousands of variables. That’s where Optiml steps in.

What Optiml Does

We created Optiml to take care of everything that makes planning difficult, while keeping it easy to use for anyone.

- Links directly to your investment accounts - so your plan is always up to date

- Models your real income, lifestyle, and goals - not generic assumptions

- Automatically calculates the optimal withdrawal strategy across RRSPs, RRIFs, TFSAs, LIRAs, non-registered accounts, and CCPCs

- Stress-tests your plan against inflation, market downturns, or different CPP/OAS start dates

- Delivers your yearly retirement plan in plain English - no jargon, just clarity

And About Financial Advisors...

We’re not here to replace your advisor. In fact, a great advisor can help you:

- Stay invested through market volatility

- Target a strong long-term return (e.g. 6%+)

- Get the right insurance to assist with estate planning

But here’s the thing: you are the one living your retirement. You know your lifestyle, your priorities, and your goals. And too often, traditional planning gets built behind closed doors using assumptions you don’t fully understand until it’s too late.

Optiml gives you control and clarity. Use it with your advisor, or use it on your own. Either way, you stay informed, empowered, and confident in your decisions.

Leaving your planning 100% to someone else is a recipe for miscommunication, missed opportunities, and goals that go unfulfilled.

Real Example: Why Order Matters

Let’s say you’re 62, retired, with:

- $700K in RRSPs

- $150K in a TFSA

- $250K in a non-registered account

Conventional wisdom says: spend the non-registered account first. Delay RRSP and CPP.

But Optiml might show that drawing some RRSP income early, while you're in a lower tax bracket, avoids huge RRIF withdrawals later and prevents OAS clawbacks. That one decision could save you tens of thousands in lifetime taxes.

That’s the difference between a rule of thumb and personalized optimization.

Why Software Beats Opinions

- Consistent: Same math every time. No hunches.

- Accurate: We use CRA tax rules and benefit formulas for your province, age, and income.

- Personalized: Based on your accounts, life goals, and timeline.

- Visual: You see the trade-offs in dollars, not vague advice.

The Bottom Line

You don’t need to decode financial jargon or chase generic advice.

You need software that works with your real numbers and shows you a smart, tax-efficient plan for your future.

That’s Optiml.